Stablecoins 101: The What, Why, and How of This Digital Asset

More than 700 million people — roughly 8.5% of the world's population — now own some form of digital currency, up from around 560 million in 2024, according to Crypto.com research and Triple-A's own data.

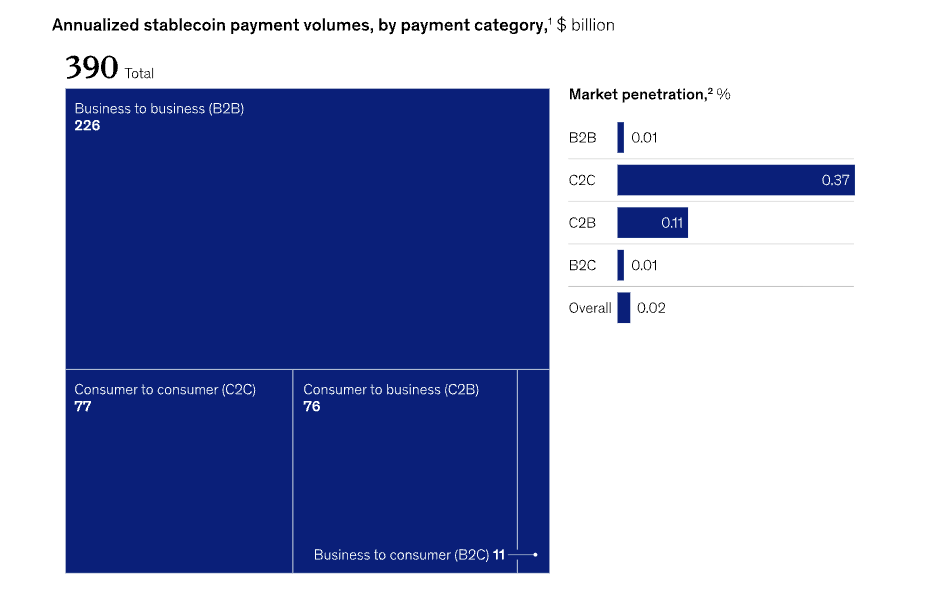

At the center of this growth is one of the most talked-about digital currencies in the industry right now: stablecoins. It’s a digital asset designed to avoid the volatility of other cryptocurrencies by pegging to real-world money, like the US dollar or euro – and it’s already exceeding $390 billion in annual payment volume.

Ahead, we’re covering what stablecoins are, the different types, business use cases, and the regulatory landscape.

What is a stablecoin?

A stablecoin is a digital currency designed to maintain a stable value, typically by tying it to a real-world asset, like the US dollar or euro. That predictability makes stablecoins uniquely suited to payments. Businesses and individuals can send, receive, and settle instantly in stablecoins knowing the value will be the same when the payment arrives as when it was sent.

Another benefit of stablecoin is that it runs on the blockchain, like Bitcoin and Ethereum. Transactions are recorded on a decentralized digital ledger, which means payments can be processed at any time – without banking hours, intermediaries, and geographic restrictions. But because stablecoin value is anchored to a familiar currency, it avoids the price volatility associated with other cryptocurrencies.

It helps to think of a stablecoin as a digital representation of existing money. Take USD Tether (USDT), which is one of the most widely used stablecoins. For every USDT token in circulation, an equivalent amount of US dollars is held in reserve by the issuer. The token itself lives on a blockchain – letting it move across borders instantly, at any time, without requiring a bank as the middleman to process the transaction – but its value is always anchored to the USD backing it.

How do stablecoins work?

Stablecoins function like local currencies, with a few distinct differences since they live on the blockchain. Here’s what’s happening under the hood of fiat-backed stablecoins (the most common type used in payments):

Who issues them

Stablecoins are often created by private companies, called issuers – think Tether (USDT), Circle (USDC), and PayPal (PYUSD). To mint a new stablecoin, the issuer collects a fiat currency (e.g. USD) and holds it in reserve, then issues an equivalent number of tokens. One dollar received, one USD-pegged token created, for example.

How they circulate

Once issued, stablecoins live on public blockchains such as Ethereum, Tron, or Solana. From there, they move freely, without a bank or payment processor. Users can send stablecoins directly to any digital wallet in the world in minutes, make payments to businesses or individuals, trade them on exchanges, or simply hold them as a dollar-denominated digital asset. Every transaction is permanently recorded on the blockchain, making payments transparent, traceable, and irreversible.

Tokens vs. network

A stablecoin token is the asset – the digital dollar itself. The blockchain network it runs on is the infrastructure used to move it, in the same way that a bank transfer and a wire transfer can both move the same currency but use different underlying systems (e.g. SWIFT for international wires, ACH for domestic bank transfers).

The same stablecoin can exist on multiple networks simultaneously: USDT, for example, is available on Ethereum, Tron, Solana, and others. The choice of blockchain network affects transaction speed, cost, and compatibility. Tron, for example, is commonly used for low-cost transfers, while Ethereum offers the widest wallet and exchange support. One thing to keep in mind, though, is that the stablecoin sender and recipient need to be using the same blockchain for the transaction to go through.

What redemption looks like

When a holder wants to convert stablecoins back to fiat currency, they return the tokens to the issuer or a participating exchange. The issuer destroys, or "burns", the tokens and releases the equivalent amount in fiat currency. For fiat-backed stablecoins, redemption is always at face value: one USDC for one US dollar.

How the peg is maintained

Similar to exchange-traded funds, stablecoins maintain price stability through market arbitrage. If a stablecoin trades below $1, traders can buy it up and redeem it with the issuer for a full dollar, pushing the price back up. If it trades above $1, new tokens can be issued and sold into the market, bringing the price back down. These corrections happen automatically and continuously, keeping the stablecoin's value aligned with its target without users needing to do anything.

Types of stablecoins

While all stablecoin shares the same goal of minimizing volatility, they can be backed by different types of assets that determine how they maintain their stability.

There are four main types of stablecoins, each with a different approach to backing, risk, and redemption:

- Fiat-backed stablecoins: Backed by real-world currency — like US dollars — held in reserve. The most widely used and trusted type of stablecoins for payments

- Crypto-backed stablecoins: Backed by other cryptocurrencies held as collateral in automated smart contracts. Since crypto prices tend to swing, the value of the crypto held in reserve exceeds the value of the tokens issued – this is called overcollateralization

- Algorithmic stablecoins: No reserves at all. Instead, the peg – meaning the fixed value target – is maintained through automated mechanisms that adjust supply based on demand. Tends to carry high risk

- Commodity-backed stablecoins: Pegged to the price of a physical asset like gold, which is stored securely by a third party. Better suited to investment use cases than everyday payments

Let’s explore each of these in more detail.

Fiat-backed stablecoins

Fiat-backed stablecoins are the most widely used type for payments and commerce. Each token is pegged 1:1 to a national currency (often the US dollar or euro) and backed by reserves held outside of the blockchain, or off-chain, in traditional, regulated financial institutions.

Those reserves typically consist of cash or highly liquid assets like short-term government securities. For every token in circulation, an equivalent amount of real-world currency is held in reserve, which means holders can redeem their stablecoins for the underlying currency at any time.

This structure makes fiat-backed stablecoins predictable, auditable, and familiar to regulators. It’s a big reason why they dominate institutional and enterprise payment use cases.

Examples of fiat-backed stablecoins:

- USDT (issued by Tether Limited, pegged to USD)

- USDC (issued by Circle, pegged to USD)

- PYUSD (issued by PayPal, pegged to USD)

- EURS (issued by STASIS, pegged to Euro)

Crypto-backed stablecoins

Crypto-backed stablecoins use other cryptocurrencies — like Ethereum — locked in automated smart contracts as collateral, rather than fiat currency. Since cryptocurrencies often experience high volatility and they’re the underlying asset in this case, crypto-backed stablecoins are typically over-collateralized. This means more value is locked in reserve than the stablecoins issued against it.

For example, to issue $100 worth of a crypto-backed stablecoin like DAI, a user needs to lock $150 worth of Ethereum as collateral. Even if the value of Ethereum drops, the stablecoin can still maintain its peg.

For payments, the practical use cases of this type of stablecoin are more limited. Because the backing assets can fluctuate in value, crypto-backed stablecoins require continuous risk management to maintain their peg. This makes them more suited to crypto-native financial applications than mainstream business payments.

Examples of crypto-backed stablecoins:

- DAI (issued by MakerDAO)

- sUSD (issued by Synthetix)

Algorithmic stablecoins

Algorithmic stablecoins maintain their peg through automated supply and demand management, rather than reserves. When demand rises, new tokens are minted; when demand falls, tokens are burned.

The appeal of this type of stablecoin is that it operates independently of any bank or reserve, looking solely to market signals to adjust supply. But in practice, algorithmic stablecoins are high-risk since they depend entirely on sustained market confidence and trust under stress, entirely without collateral.

The risks of this model became clear in 2022, when the collapse of TerraUSD (UST) wiped out over $400 billion in value almost overnight. Since it was algorithmic, UST maintained its peg not through reserves, but through an algorithmic relationship with a sister token, LUNA. When confidence in UST weakened, the mechanism designed to stabilize it also acted in reverse, responding to the negative market signals: it triggered a feedback loop that sent both tokens to near zero, erasing billions in market capitalization.

Example of algorithmic stablecoin:

- AMPL (issued by the Ampleforth protocol)

Commodity-backed stablecoins

Commodity-backed stablecoins are pegged to the value of a physical asset, typically gold, instead of a currency. Each token represents ownership of a specific quantity of that commodity, which is held in a secure vault by a third-party custodian. One token of PAX Gold (PAXG), for example, represents one troy ounce of physical gold stored in a Brink's vault in London.

This type of stablecoin offers a way to access and transfer commodity exposure digitally, without needing to physically hold or transport the asset. But they don’t act like currency – stablecoin value fluctuates based on the underlying commodity instead. This makes them better suited to treasury or investment strategies than to everyday payment use cases.

Examples of commodity-backed stablecoins:

- PAXG (issued by Paxos, pegged to gold)

- XAUt (issued by Tether, pegged to gold)

Use Cases for Stablecoins in Business

Global businesses are rapidly adopting stablecoins because they solve specific, expensive problems that organizations deal with every day:

- High international payment processing fees

- Slow cross-border payouts

- Inaccessible customer markets

- Fragmented treasury operations

Accept international payments faster and at lower cost

Businesses operating globally face the same fundamental problem regardless of whether payments happen by card at checkout or via wire transfer and invoice: cross-border transactions are slow, expensive, and hard to predict.

For checkout-driven businesses, like eCommerce platforms and gaming platforms, every international card payment carries processing fees that average around 2% per transaction in the US, before additional charges, currency conversion, or chargeback exposure. For a platform processing $10 million in cross-border card payments annually, that's $200,000 or more absorbed in fees alone. And when a customer disputes a card transaction, the merchant typically loses both the revenue and the goods.

For businesses collecting cross-border payments via invoice or pay-by-link, like importers/exporters and B2B SaaS providers, the default payment is by international wire transfer. SWIFT wires take two to five business days to settle, carry unpredictable fees, and are difficult to track. For a professional services firm waiting on a $500,000 payment from an overseas client, the difference between a five-day wire and same-day stablecoin settlement has a major impact on cash flow.

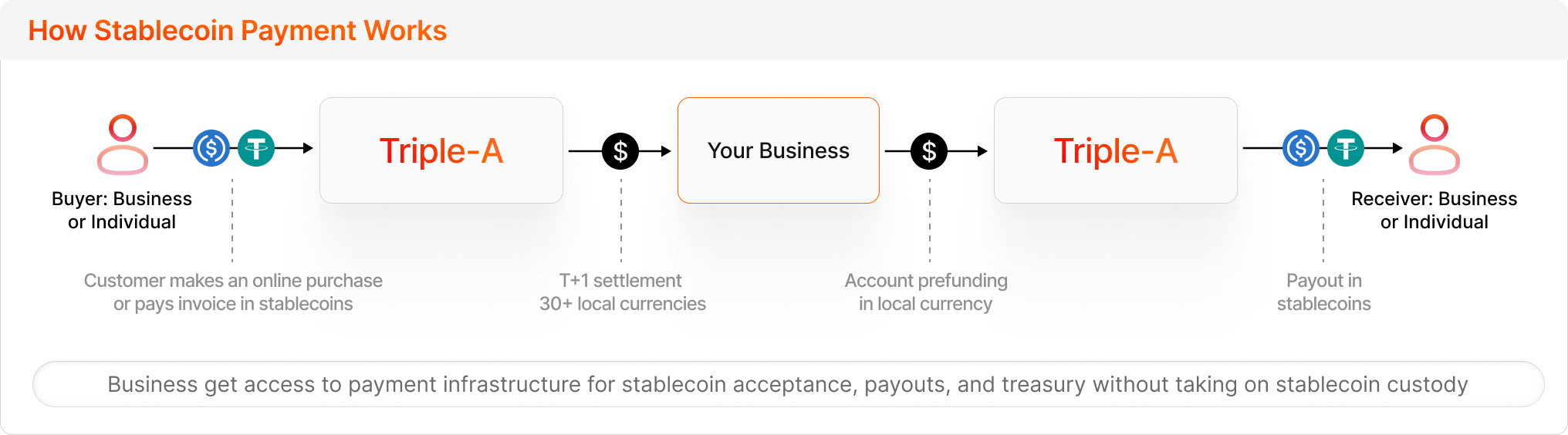

Stablecoins address both payment situations. Cross-border payments settle in minutes rather than days, at a fraction of the cost of either a card transaction or a SWIFT wire transfer – with full transaction visibility from the moment payment is sent. And since stablecoin transactions are irreversible on the blockchain, chargeback risk is eliminated entirely. Businesses can accept stablecoin payments without holding or managing crypto directly (customers pay in stablecoins, merchants receive the equivalent value in local currency) by using licensed providers like Triple-A, so the operational complexity typically associated with digital currencies doesn't apply.

Send payment globally, in real-time

Paying contractors, freelancers, creators, and suppliers across borders is one of the most operationally complex and costly things that businesses do. Most rely on SWIFT wires or local bank rails that are slow, expensive, and difficult to track. FX spreads and intermediary fees eat into the amounts recipients actually receive, and a contractor in Southeast Asia or West Africa may wait days for a payment that was sent exactly on schedule.

According to the World Bank, the global average cost of sending money internationally was 6.49% in Q1 2025, with bank transfers averaging as high as 14.55%. For platforms sending high volumes of payouts, those fees quickly add up.

Stablecoins offer a faster, cheaper, and more accessible alternative. Payouts settle in minutes rather than days, operate 24/7, and can reach recipients in markets where traditional banking infrastructure is limited – including across APAC, MENA, and Latin America where demand for dollar-denominated digital payments is high. Transaction costs typically come in well under 1%, and recipients without access to a traditional bank account can receive USD-equivalent payments directly to a digital wallet.

For the platform sending the payouts, the process is straightforward: send payouts in stablecoins, which are converted to local currency on the recipient's end.

Reach customers in emerging markets

Over 700 million people globally now hold some form of digital currency. Many of these individuals are in Asia, the Middle East, Latin America, and Africa, where there’s currency instability and limited access to traditional banking have driven demand for dollar-denominated activities.

The numbers directly reflect this demand. According to research by Castle Island Ventures:

- 69% of consumers in emerging markets have converted local currency into stablecoins at least once

- 47% use stablecoins primarily to store wealth in US dollars

This represents a practical business opportunity that traditional payment infrastructure struggles to serve. Customers in these regions may not have reliable access to international credit cards, but many already hold and transact in stablecoins.

For businesses looking to expand into these emerging markets, accepting stablecoins is a practical path forward. Rather than integrating multiple local payment methods market by market, stablecoin offers a single rail that works across borders and meets customers with the payment method they’re already using.

Simplify treasury and liquidity management

Managing liquidity across multiple currencies, banking relationships, and time zones creates constant operational drag. Funds sit idle waiting for banking windows to open, FX costs accumulate on transfers between entities, and cash positions across accounts are difficult to track in real time.

Stablecoins provide a more efficient liquidity layer. By operating 24/7 on the blockchain, stablecoins enable global treasury teams to:

- Move funds between entities or geographies in minutes, not days

- Reduce FX exposure by consolidating liquidity in dollar–denominated stablecoins and converting to local currency only when needed

- Track positions across accounts to get real–time cash visibility without waiting for end-of-day reconciliation

- Reduce reliance on fragmented multi-bank structures across jurisdictions

And now there’s a stablecoin model gaining serious traction in cross-border treasury and liquidity operations: the stablecoin sandwich. In this cross-border payment structure, the sender pays in their local currency, the funds travel across a blockchain as a stablecoin, and the recipient receives payment in their own local currency – with the stablecoin layer operating entirely behind the scenes. By using a compliant stablecoin payment provider, like Triple-A, to turn fiat currency into stablecoin, neither side needs to manage crypto directly.

For treasury teams, this means moving funds between entities across different currencies and geographies in minutes, at a fraction of the cost of traditional intercompany transfers, without taking on direct exposure to digital assets. According to a recent EY survey, 44% of institutions cited cross-border treasury and liquidity management as their top stablecoin use case.

Stablecoin Payments in Practice

Stablecoin payments can be adopted in different ways. A business can build finance teams and compliance capabilities that let it accept stablecoins from customers, hold the stablecoins in a blockchain wallet, and payout vendors and suppliers in stablecoins.

Regulated payment providers also offer an alternative option — businesses can accept and send stablecoin payments while operating entirely in local currencies. The payment provider manages conversions between stablecoins and local currencies, letting the business accept and send stablecoins without holding digital assets on their books.

The latter model is an increasingly popular model for enterprises, allowing them to participate in the stablecoin economy without the need to build new teams and processes or worry about compliance implications.

Are stablecoins regulated?

As stablecoins have grown from niche digital tools into widely used payment instruments, regulators across major economies have moved to define how they should be supervised. While frameworks differ by jurisdiction, a clear theme is emerging: stablecoins used for payments must be fully backed by high-quality reserves, issuers must meet disclosure and governance standards, and holders must have enforceable redemption rights.

Here is where the major jurisdictions stand today regarding stablecoin regulation.

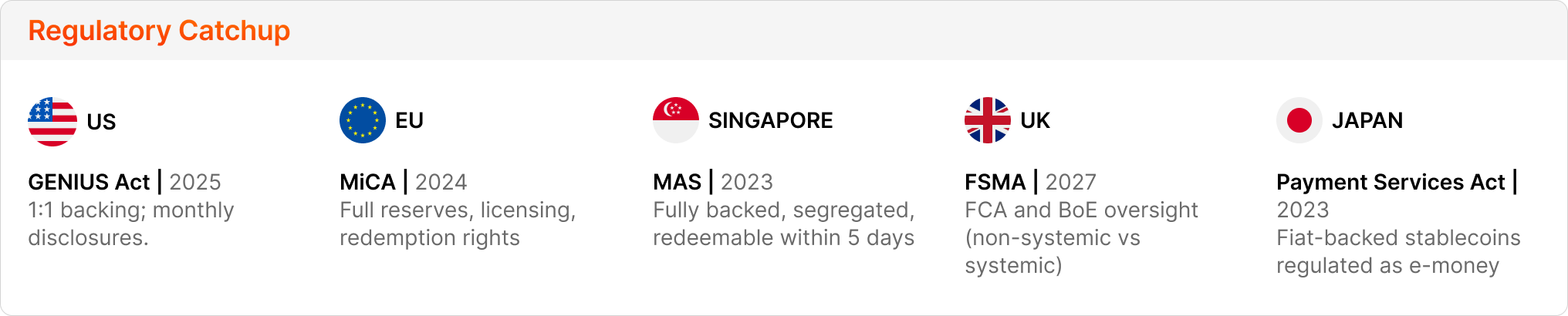

United States: GENIUS Act

The US now has its first dedicated federal framework for stablecoins: The GENIUS Act, which was signed into law in July 2025. The GENIUS Act establishes clear requirements for payment stablecoin issuers:

- Tokens must be backed 1:1 by highly liquid assets, such as cash or short-term government securities

- Reserves must be held separately from operating funds

- Issuers must publish monthly disclosures on reserve composition

The legislation brings stablecoins under federal supervision for the first time, replacing a fragmented patchwork of state-level money transmitter licenses.

European Union: MiCA

The EU's Markets in Crypto-Assets Regulation (MiCA) is the most comprehensive stablecoin framework currently in force globally. In effect since June 2024, MiCA requires stablecoin issuers to:

- Obtain a license

- Maintain full reserve backing

- Segregate reserve assets from operating funds

- Provide clear redemption rights to holders

MiCA defines two categories of stablecoins: e-money tokens (EMTs), pegged to a single fiat currency, and asset-referenced tokens (ARTs), which reference a broader basket of assets.

Singapore: MAS Framework

Singapore's Monetary Authority of Singapore (MAS) introduced a dedicated regulatory framework for single-currency stablecoins in 2023. Qualifying stablecoins must be:

- Fully backed by low-risk, liquid reserve assets

- Held separately from the issuer's own funds

- Redeemable at par value within five business days

Only stablecoins meeting these requirements may carry the "MAS-regulated stablecoin" designation, giving businesses and consumers a clear signal of regulatory compliance.

United Kingdom: FSMA Framework

The UK is integrating stablecoins into its existing payments regulatory framework through amendments to the Financial Services and Markets Act that are set to be enforced in October 2027.

Under the Act, oversight is split between two institutions:

- Non-systemic stablecoins (those that are small enough not to pose a risk to broader financial stability) fall under FCA regulation alone

- If a stablecoin grows large enough to be designated systemic by HM Treasury, it moves into a joint regime where the Bank of England's rules apply alongside the FCA's

The FCA recently selected four companies – Revolut, Monee Financial Technologies, ReStabilise, and VVTX - to test stablecoin products in its regulatory sandbox. The findings will feed directly into the UK's final stablecoin policy.

Japan: Payment Services Act

Japan was among the first countries to establish a stablecoin framework. Under amendments to the Payment Services Act (PSA) that came into force in June 2023, fiat-backed, redeemable stablecoins are regulated as "electronic payment instruments" (EPIs).

The framework continues to evolve. A 2025 amendment relaxed reserve requirements for stablecoin issuers, permitting up to 50% of reserves to be held in low-risk assets such as short-term government bonds or early-cancellable deposits. Japan's first regulated yen-backed stablecoin, JPYC, was also approved in 2025.

What to Watch Out For: Risks and Considerations

No payment technology is without trade-offs. Businesses evaluating stablecoins should be aware of the following:

Our View

The risks of stablecoins are manageable and significantly lower than the risks of not adapting to modern payment infrastructure. Businesses that choose a licensed, regulated infrastructure partner, use audited fiat-backed stablecoins, and implement basic internal controls can move money globally with confidence.

Ready to start accepting crypto payments globally? Triple-A operates with flexible settlement options. Contact us today to find out more.

FAQs

What is a stablecoin, and how is it different from other cryptocurrencies?

A stablecoin is a digital currency designed to hold a fixed value, rather than fluctuate in price. It’s typically pegged 1:1 to a fiat currency, like the US dollar or another national currency. Most cryptocurrencies like Bitcoin or Ethereum are speculative assets whose value changes constantly based on market demand. Stablecoins are built for a different purpose: to function as a reliable medium of exchange. They run on the same blockchain infrastructure, giving them the speed and accessibility advantages of crypto, but their value is anchored to something familiar and predictable.

Are stablecoins safe to use for business payments?

Absolutely. Fiat-backed stablecoins, which are the type of stablecoin often used in business payments, are backed by real-world reserves such as cash or short-term government securities, held in regulated financial institutions. For businesses, the safest approach is to work with a licensed payment provider that handles stablecoin acceptance and settlement on your behalf, rather than managing stablecoin holdings directly. This way you access the benefits (speed, cost, reach) without direct exposure to the asset.

Which stablecoin is best for payments?

For payments, fiat-backed stablecoins are the only practical option. Among those, USDT (Tether) and USDC (Circle) dominate by volume and liquidity. USDC is generally considered the more transparent of the two, with monthly independent audits of its reserves. USDT has the largest market cap and widest acceptance globally, particularly in emerging markets. For euro-denominated payments, EURS (issued by Stasis) is the most widely used option. The right choice depends on your payment corridors, your customers' preferences, and your settlement currency requirements.

Do businesses need to hold or manage crypto to accept stablecoin payments?

No. Businesses can accept stablecoin payments and receive settlement in their local fiat currency, without holding or managing any cryptocurrency directly. Licensed payment providers can handle the conversion, compliance, and settlement on the merchant's behalf. This means the operational complexity normally associated with crypto, like wallets, private keys, and price exposure, does not apply. For most businesses, accepting stablecoins is like adding a new payment method.

What are stablecoins used for in cross-border payments?

Stablecoins are increasingly used to solve two specific cross-border payment problems: accepting payments from international customers, and sending payouts to contractors, suppliers, or partners abroad. In both cases, they offer a faster and cheaper alternative to the default options, international card transactions and SWIFT wire transfers, which are slow, expensive, and unpredictable in cost. Stablecoin transactions settle in minutes, operate 24/7, provide full transparency into the transaction, and typically cost a fraction of a percent, compared to average global remittance costs of 6.49% reported by the World Bank in Q1 2025.