Types of Stablecoins: A Practical Guide for Modern Payments

Stablecoins are being adopted globally as a new backbone for modern payment systems. They help businesses move money faster, settle transactions across borders, and access local currencies more efficiently. While they are often discussed alongside cryptocurrencies, stablecoins serve a very different purpose: they are designed for stability, settlement, and payments, not for speculation.

Stablecoin supply has grown from under $10 billion to over $300 billion in roughly five years, according to Artemis, with over $136 billion in stablecoin payments settled between January 2023 and August 2025, reaching an annualized run rate of approximately $118 billion.

Chainalysis data further illustrates the scale of growth: between June 2024 and June 2025, USDT alone processed hundreds of billions of dollars per month — at times exceeding $1 trillion in monthly transaction volume. Other stablecoins, such as PaypalUSD (PYUSD) and EUR-denominated tokens, are growing from smaller bases.

With this growth, regulators, financial institutions, and payment providers are looking beyond adoption and focusing on design — how stablecoins are built and what tradeoffs they make. Understanding the different types of stablecoins helps explain why some models have gained institutional traction, while others remain limited to niche or experimental use cases.

What are stablecoins?

A stablecoin is a digital currency designed to maintain a stable value relative to a reference asset — most commonly a national currency such as the US dollar or euro.

For businesses and payment providers, stablecoins are best understood as:

- A way to process settlements, not as an investment

- Digital versions of existing local currencies, not as replacements

- Technology that supports payment infrastructure, not as a speculative cryptocurrency

This answers a common question: do stablecoins go up in value?

In normal conditions, they are not intended to. Stablecoins used for payments prioritize predictability over price appreciation.

Why stablecoins exist in payment systems

Traditional payment systems were not built with a globally connected, internet-native economy in mind. As a result, cross-border transfers can be slow, costly, and operationally complex, with multiple correspondent banks involved.

Stablecoins offer an alternative settlement layer. With stablecoins:

- Funds can be moved globally in seconds instead of days

- Transactions can be executed outside banking hours

- Settlement can be made without accounts in every jurisdiction

Crucially, stablecoins are most effective when paired with conversion into local currencies such as USD, EUR, GBP, and others. They allow businesses to benefit from faster settlement without changing how they account, price, or report.

Digital currency ownership and the driver for stablecoin growth

Stablecoin adoption is tied to a broader trend: the normalization of digital currencies.

According to Triple-A’s data, global digital currency ownership reached approximately 6.8% of the population (over 560 million people) in 2024. In 2026, that number has grown to 700 million people — 8.5% of the population.

While this includes all digital currencies, it helps explain why demand for stablecoin-based payments has increased. As more consumers and businesses hold digital value, the way that value can be used naturally evolves.

Stablecoins sit at the intersection of this trend and traditional payments, acting as a bridge between digital ownership and practical, spendable money. This is reflected in Triple-A’s transactions, with over 90% of our payment volume being processed in stablecoins.

Types of stablecoins: an overview

There are four commonly recognized types of stablecoins:

- Fiat-backed stablecoins

- Crypto-backed stablecoins

- Algorithmic stablecoins

- Commodity-backed stablecoins

Each type reflects a different approach to stability, risk management, and redemption, and suits different payment contexts.

1. Fiat-backed stablecoins

Fiat-backed stablecoins track the value of a specific currency, such as USD or EUR, and are backed by off-chain reserves. These reserves are held outside the blockchain, in traditional financial institutions such as banks and custodians.

Reserve backing means that, for every stablecoin in circulation, the issuer holds assets to match its value. These reserves are typically:

- cash or cash equivalents, and/or

- short-term, highly liquid government securities

Simply put, a fiat-backed stablecoin is a digital claim on real-world money. When a holder redeems the stablecoin, the issuer is expected to return the equivalent value in the underlying currency.

This explains why fiat-backed stablecoins function as reliable settlement instruments.

Why regulators prefer fiat-backed stablecoins

Fiat-backed stablecoins are among the most “regulatable” of the stablecoins. They’re designed to resemble digital money, with clear backing and clear redemption.

In the United States, proposed legislation such as the GENIUS Act aims to create a federal framework for fiat-backed stablecoins, focused on supervision, safety, and consumer protection. While some details are still being finalized, the direction is clear: stablecoins for payments should behave like digital money, not like high-risk financial products.

Regulatory momentum is also building on both sides of the Atlantic. As the United States moves forward with the GENIUS Act to strengthen oversight in the world’s largest stablecoin market, the European Union has taken a similarly important step through its MiCA regulatory framework. Under MiCA, stablecoin issuers must fully back their stablecoins with real money, keep those funds separate from their own operating money, and clearly allow users to redeem stablecoins for cash. These rules are designed to ensure issuers can always return money to users, even during times of stress.

The risks of stablecoins, and how the system addresses them

Fiat-backed stablecoins are not risk-free. They depend on issuer governance, reserve management, and operational resilience. However, these risks are familiar to traditional finance and are managed using established tools: regulatory supervision, independent audits, reserve disclosures, segregation of funds, and diversified custodial arrangements.

For payment systems, this familiarity matters. Risks that are understood, measurable, and supervisable are far easier to integrate than risks that rely primarily on market confidence.

2. Crypto-backed stablecoins

Crypto-backed stablecoins are collateralized, which means other cryptocurrencies are held as a safety deposit, or collateral. The collateral is locked into automated systems called smart contracts, and is typically of higher value than the stablecoins issued. This so-called over-collateralization helps absorb price swings, and because most of the collateral sits on-chain, the system is relatively transparent and verifiable.

However, from a payments perspective, the trade-offs are significant. Because the backing assets are volatile, stability depends on continuous risk management and favorable market conditions. Sudden price movements can trigger liquidations, increasing operational complexity.

As a result, crypto-backed stablecoins tend to be more suited to crypto-native environments than to mainstream payment and settlement use cases.

3. Algorithmic stablecoins

Algorithmic stablecoins use supply-and-demand mechanisms to keep their prices stable, rather than being backed by reserves.

The appeal of this system is clear: a stable digital currency independent of banks, custodians, or reserves can use algorithms to expand or contract supply based on market signals. This is often supported by a secondary token that absorbs volatility.

In practice, however, this design demands a lot of confidence. Without redeemable assets to anchor the value, the system depends on the trust of participants that the mechanism will work under stress.

This vulnerability was starkly illustrated in 2022 by the collapse of TerraUSD (UST) and the associated Luna ecosystem. When confidence weakened, the stabilization mechanism failed to restore the peg and instead accelerated its breakdown. Billions in value were lost, and the episode became a reference point for regulators and institutions globally.

The lesson was straightforward: payment systems must remain reliable under adverse conditions. Algorithmic models have struggled to meet that requirement.

4. Commodity-backed stablecoins

Commodity-backed stablecoins are linked to physical assets such as gold.

These tokens provide digital access to commodities and can be useful for investors or treasury strategies seeking exposure to real assets. Holders can typically redeem those tokens for commodities held in secure vaults by third-party custodians.

Commodity-backed stablecoins are not designed to behave like currencies, however. Commodity prices fluctuate, making redemption processes more complex, and liquidity is often lower than for fiat-denominated instruments. As a result, these stablecoins function more as digitized commodities than as payment instruments.

Common stablecoin examples

Widely referenced stablecoins include:

- Fiat-backed: USDT, USDC, PYUSD, GUSD, USDP, TUSD, EURS

- Crypto-backed: DAI

- Commodity-backed: PAXG, XAUT

Since all stablecoins are designed to remain stable, comparisons between competing stablecoins (e.g,USDT vs USDC) typically focus less on price behavior and more on factors such as:

- Governance: Who controls the stablecoin, how decisions are made, and who is accountable if something goes wrong.

- Reserve transparency: How clearly the issuer discloses the assets backing the stablecoin, how often it reports on those reserves, and whether those reports are independently audited and verified.

- Regulatory posture: Whether the issuer operates under a clear legal framework, holds the relevant licenses, and meets payment and financial oversight requirements.

- Corridor availability: How easily the stablecoin can be used and exchanged across different countries and currencies, including whether there is sufficient liquidity and reliable on/off-ramps.

How businesses actually use stablecoins in payments

For most businesses, stablecoins are not held as long-term assets. They act as a transactional layer, with value ultimately settling into local currencies.

This is especially true in cross-border trade, where stablecoins can reduce delays and costs between counterparties in different banking systems. Triple-A’s analysis of stablecoin-based cross-border payments for importers and exporters explains how this works in practice.

For merchants considering digital currency, Triple-A’s practical guide to accepting digital payments outlines how to do so while minimizing volatility exposure.

In both cases, the key idea is simple: stablecoins drive the transaction, while the business sees the result in its local currency.

A practical takeaway for payment decision-makers

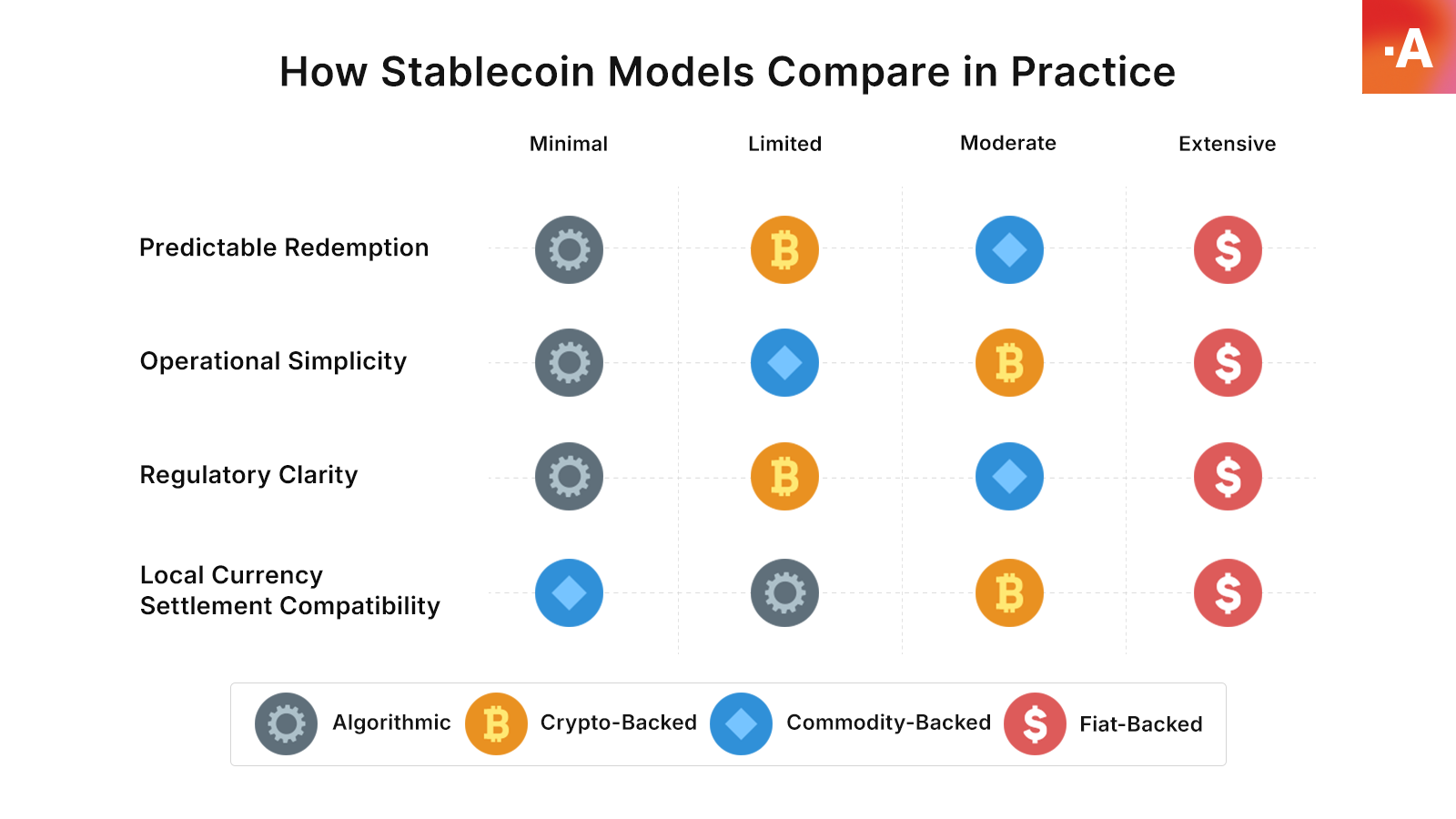

Looking at stablecoins in practical terms, it becomes much clearer. Different payment models solve different problems, but on the whole, they reward designs that emphasize:

- Predictable redemption: Knowing what you will receive and how when you exit a stablecoin, especially under market stress.

- Operational simplicity: Integrating, managing, and operating stablecoins easily within your existing payment, treasury, and accounting workflows.

- Regulatory clarity: Clearly understanding how the stablecoin is addressed, permitted, and supervised under existing or emerging payment regulations.

- Compatibility with local currency settlement: Easily converting the stablecoin into local currencies (such as USD or EUR) at scale for real-world business use.

Here’s how the different types of stablecoin perform against these criteria.

Fiat-backed stablecoins perform best in payments because their payment infrastructure prioritizes reliability over experimentation.

Do businesses need to hold stablecoins on their balance sheet?

Not necessarily. Many businesses use stablecoins purely as a transactional or settlement layer, and convert them into local currencies shortly after the payment has been received. This allows companies to benefit from faster settlement and broader payment reach without taking on long-term exposure to digital assets.

Payment providers increasingly support this model, enabling stablecoin acceptance while keeping accounting, treasury, and reporting processes aligned with traditional currency operations.

Ready to start accepting crypto payments globally? Triple-A operates with flexible settlement options. Contact us today to find out more.

FAQs

What are the top five stablecoins?

There is no single “official” ranking, as stablecoins can be compared by different metrics such as market capitalization, transaction volume, or usage in payments.

That said, USDT and USDC consistently account for the majority of global stablecoin transaction volume. Other widely referenced stablecoins include PYUSD, USDP, and DAI — each serving different market segments.

When it comes to payments, liquidity, corridor availability, and ease of conversion into local currencies tend to matter more than headline market cap.

using different metrics, such as market capitalization, transaction volume, or payment usage.

What is the safest stablecoin for payments?

From an institutional and payments perspective, stablecoins with clear redemption rights and high-quality reserve backing are generally considered the safest to use. These are designed to not only hold value, but also provide confidence to the holder when redeemed. That does not mean they are “risk-free,” but rather that the risks are well understood, measurable, and manageable using established financial controls.

Payment providers and businesses typically evaluate factors such as reserve composition, issuer governance, regulatory oversight, and operational reliability when assessing suitability.

How many types of stablecoins are there?

Globally, there are hundreds of types of stablecoins, many of which are small, experimental, or limited to specific platforms. However, only a relatively small number are used at meaningful scale for payments, settlement, or treasury operations.

In practice, most real-world payment activity is concentrated among a handful of stablecoins, such as USDT, USDC, and Paypal USD, with strong liquidity and established infrastructure.

What stablecoins are backed by USD?

Many stablecoins are designed to track the US dollar, including USDT, USDC, PYUSD, GUSD, USDP, and TUSD.

However, “backed by USD” can mean different things in practice. Some issuers hold reserves primarily in cash, while others use a mix of cash equivalents and short-term government securities.

For businesses, reviewing reserve disclosures and redemption terms is more important than relying on labels alone. In most cases, these stablecoins are backed by reserve assets in US dollars or equivalents, such as cash held in banks or short-term US Treasury securities. The exact composition varies by issuer, but their objective is the same: to ensure each token can be redeemed for one US dollar under normal conditions.

Are stablecoins regulated?

Stablecoin regulation is evolving rapidly.

In the European Union, MiCA establishes a formal framework for stablecoins used in payments, including requirements around reserve backing, governance, and redemption.

In the United States, legislation such as the GENIUS Act aims to create a federal framework for payment stablecoins, with oversight and safeguards intended to support consumer and financial stability.

While details vary by jurisdiction, the regulatory direction is increasingly clear: stablecoins used for payments are expected to meet higher standards than speculative digital assets.