Multicurrency Accounts built to connect local collection and global payouts

Collect EUR locally. Move funds globally

Collect EUR locally without being local

Connect collections directly to global payouts

Reconcile with named accounts

Reduce transaction cost and complexity

Account infrastructure built for cross-border money movement

Triple-A Multicurrency Accounts connect EUR collection directly to stablecoin and local payout infrastructure, so your business can move funds across borders without a local entity.

No local entity required

Named IBAN in your business name

EU payment rail acceptance

Instant funds availability

Designed for businesses collecting in Europe and paying out worldwide

Triple-A Multicurrency Accounts are designed for global businesses that need to collect in EUR and pay out globally, with less cost and complexity.

B2B companies selling into Europe

Receive EUR through local payment rails and move funds globally into a bank account, stablecoins, or local currency payouts.

Marketplaces and platforms

Accept EUR from European customers and pay out to sellers, freelancers, suppliers, or users across 70+ countries.

.png)

PSPs, wallets, EMIs, and banks

Embed EUR collection and global payout capabilities into your own platform through Triple-A's single infrastructure layer.

How it works

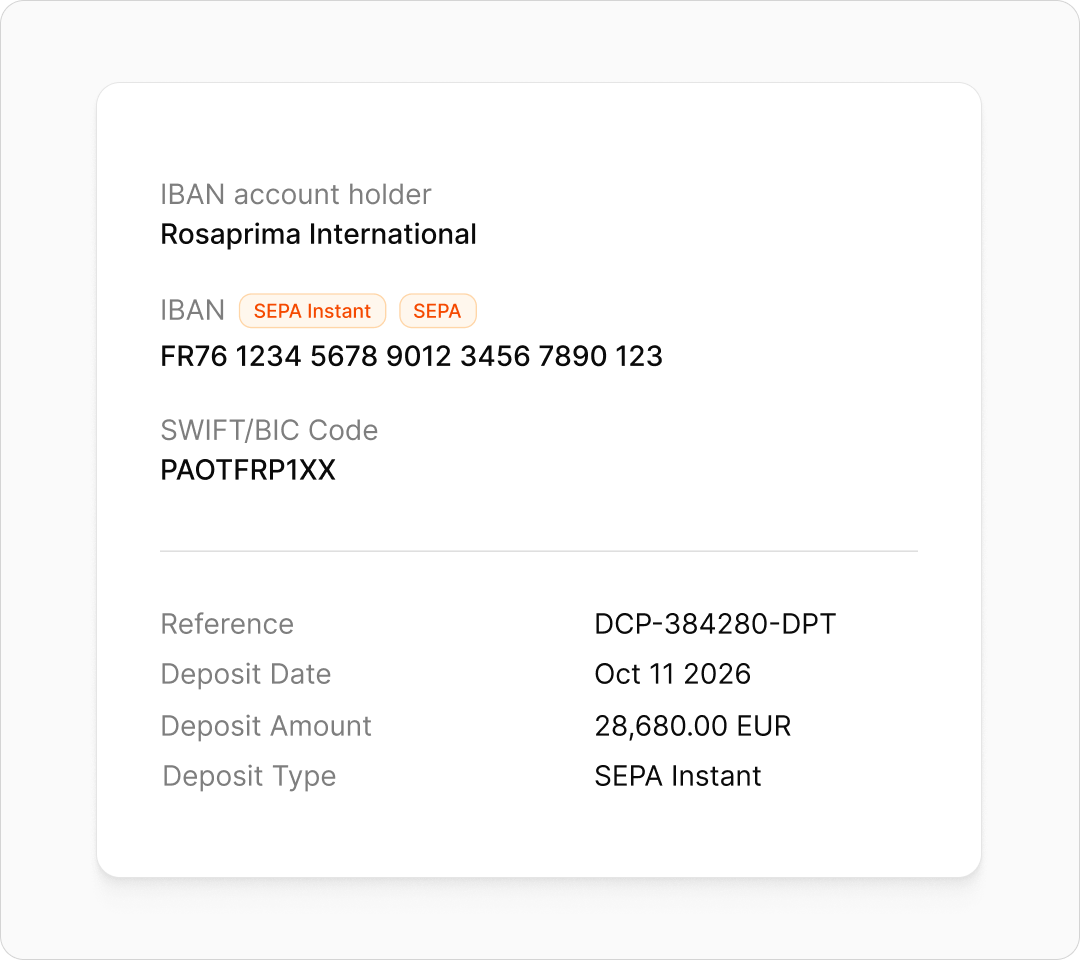

Set up your Multicurrency Account

Complete onboarding and compliance checks with Triple-A to get a named EUR IBAN, with no local entity required

Collect EUR through local rails

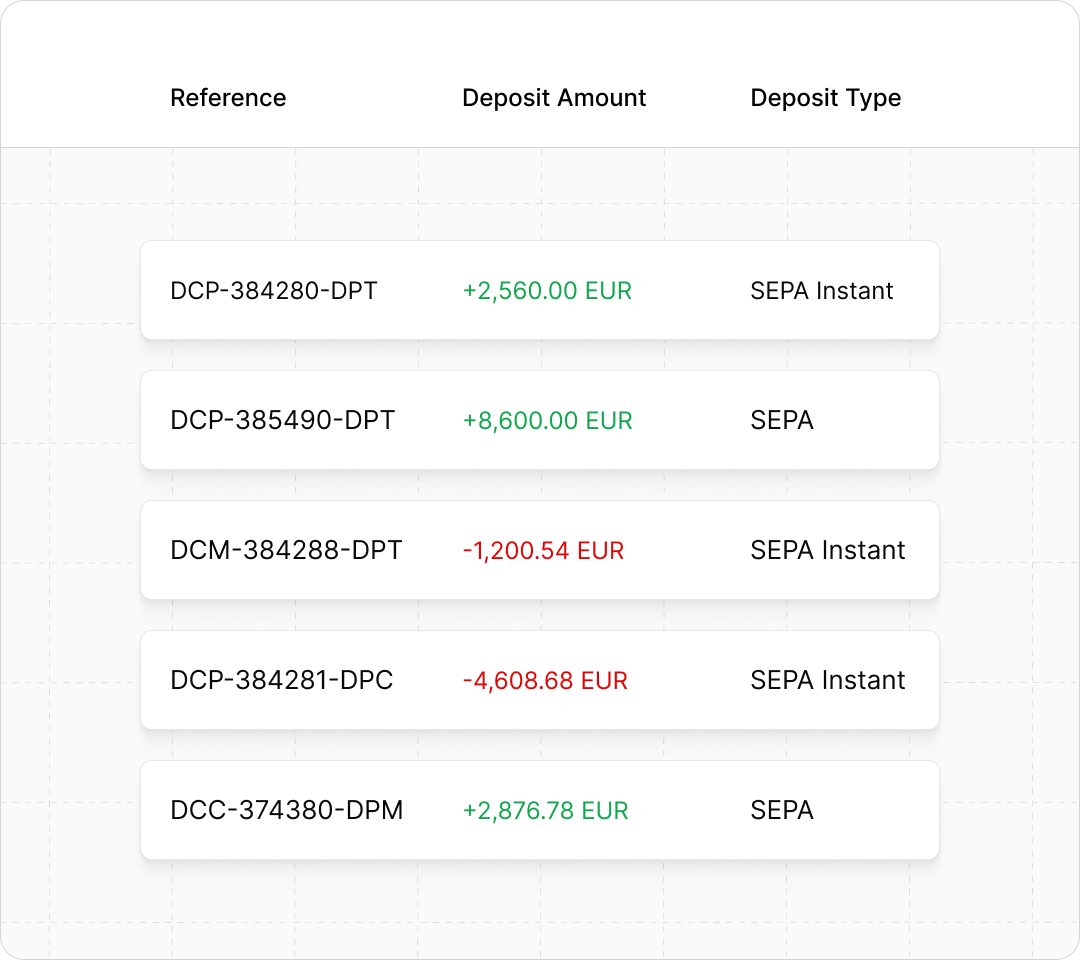

Customers pay into your named account through SEPA or SEPA Instant.

.png)

Access funds in one connected system

Collected EUR is immediately available within Triple-A's connected payment infrastructure.

.png)

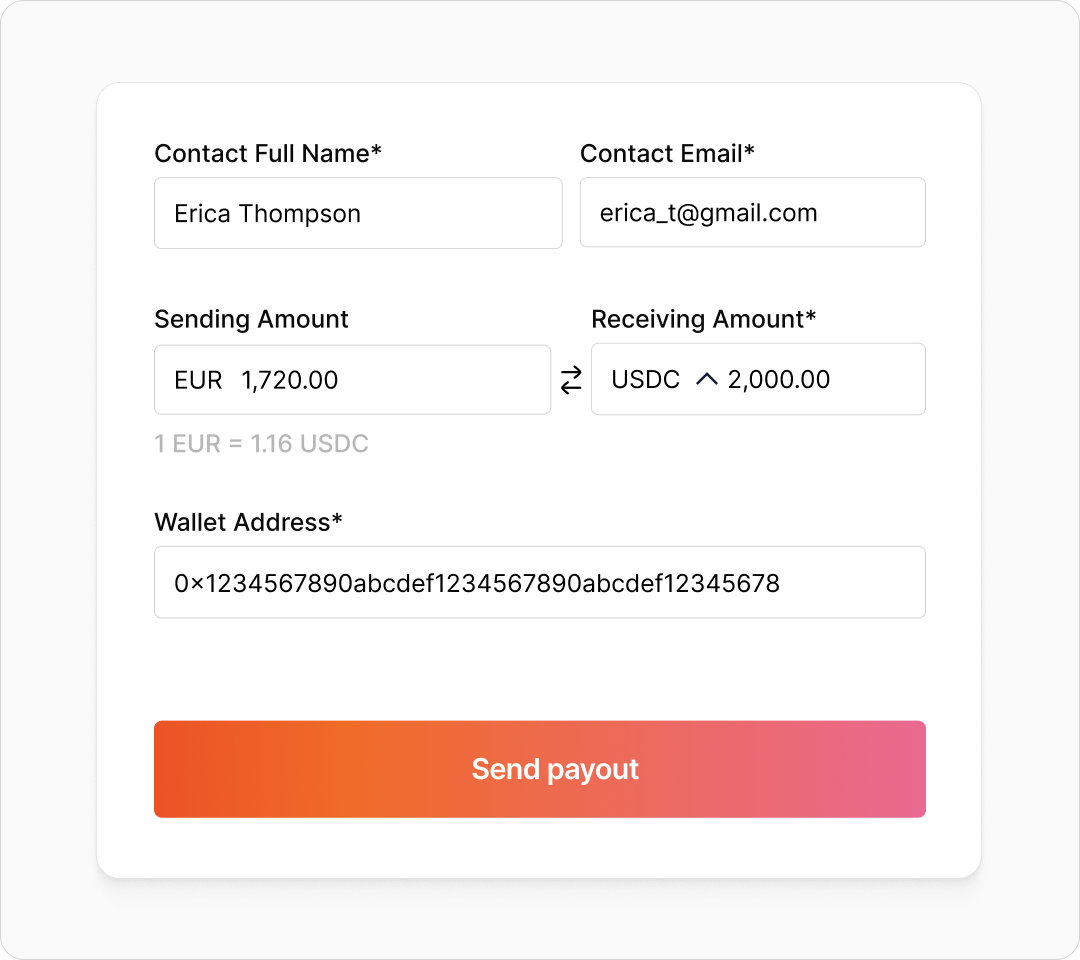

Move funds globally

Send funds to a bank account, stablecoin wallet, or local currency payout across 70+ countries.

.png)

FAQs

What is a Triple-A Multicurrency Account?

A Triple-A Multicurrency Account is a named business account that lets you collect EUR through SEPA and SEPA Instant and move funds globally through one connected system without setting up a local entity or bank account. Unlike stablecoin-focused providers that lack strong local currency collection capabilities, Triple-A Multicurrency Accounts combine EUR collection with broad payout coverage across stablecoins and 30+ local currencies in 70+ countries.

Do I need a local entity to open a multicurrency account with Triple-A?

No. You can open a named account and access local banking rails without incorporating in that market. For example, a business based in Asia or Latin America can collect EUR from European customers through local payment rails without setting up an EU entity, and move those funds globally through Triple-A's connected payout infrastructure.

What makes a Triple-A Multicurrency Account different from other account providers?

Most multicurrency account providers focus on holding and managing balances across currencies, with collection and payouts operating as separate steps. Triple-A directly connects local currency collection to global payout infrastructure within a single, unified system, so funds move through your business rather than sitting in an account. The key differentiator with Triple-A Multicurrency Accounts is built-in access to stablecoin rails alongside 30+ local currencies, giving businesses a payout network that traditional multicurrency account providers don't offer.

Who are Triple-A Multicurrency Accounts designed for?

Triple-A Multicurrency Accounts are designed for global businesses that need a single solution to collect, hold, move, and pay out funds across stablecoin, EUR and local currencies. Most stablecoin providers lack strong local currency collection, while traditional account providers don't offer stablecoin rails. Triple-A bridges both by combining EUR collection via SEPA and SEPA Instant with payout coverage in stablecoins and 30+ local currencies across 70+ countries. If your business collects in one market and pays out in another, Triple-A Multicurrency Accounts provide that single, unified bridge.

Does Triple-A allow PSPs, digital wallets, EMIs, and banks to offer Multicurrency Accounts to their own clients?

Yes. Triple-A provides the infrastructure layer that enables PSPs, digital wallets, EMIs and banks to add EUR collection and global payout capabilities to their own platforms. This integration allows financial institutions and payment providers to offer their clients named EUR IBANs, SEPA collections, and payouts through stablecoins or 30+ local currencies across 70+ countries, without building or managing the underlying infrastructure themselves.

How quickly can I access funds after collection?

Funds collected through local payment rails are available for payout almost immediately. Once a payment lands in your Triple-A Multicurrency Account, it can be routed directly into stablecoin or local currency payouts in seconds. There are no batch processing cycles, no waiting for banking windows, and no holding periods before funds can be moved.

How are EUR collections made through Triple-A’s Multicurrency Accounts?

EUR collections are made through SEPA and SEPA Instant using EUR IBANs. Businesses can receive EUR payments from European customers through local bank transfer rails. Once funds are collected, they can be used for bank settlement, stablecoin transfers, or local currency payouts across 70+ countries, through Triple-A’s connected payout network.