Top Stablecoins for Business Payments in 2026

Top Stablecoins for Business Payments in 2026

If your business is moving toward stablecoin payments in 2026, it can be a challenge to know which option is the best fit. There are currently over 200 options, each with its own pros and cons.

That said, over 90% of fiat-pegged stablecoins are pegged to the US dollar, and the top five account for the vast majority of real commercial payment volume. That helps narrow the field.

Understanding the different types of stablecoins and what they’re used for is important. For example, stablecoins backed up by local currencies are usually the strongest starting point for business payments because their value is supported by cash, Treasuries or similar assets. Crypto-backed and synthetic stablecoins can be useful, but can be riskier than fiat-backed stablecoins.

If you manage cross-border payments, supplier settlements, or global treasury operations, what matters most is that the stablecoin you opt for is ready for enterprise use. You need to know that it is regulated, transparent, liquid, and available on the rails you already run on.

This guide covers the top stablecoins for business payments in 2026 and what makes each one a fit for different use cases.

New to stablecoins? Start with Stablecoins 101.

What Makes a Stablecoin Good for Business Payments?

Not every stablecoin is built to do the same job. Before evaluating the options, you need to know what matters when you use stablecoins for commercial activity as well as for trading.

Here are the key areas to consider and the questions to ask:

Reserve transparency

Is the stablecoin backed 1:1 by cash, Treasuries, or other high-quality assets? Are those reserves independently attested on a regular basis?

This matters because the value of a stablecoin depends on the quality and transparency of its reserves. If those reserves are opaque, illiquid, or unverified, you’re taking on risk you probably don’t know about.

Regulatory standing

Does the issuer operate under a recognized regulatory framework, such as NYDFS, MiCA, or MAS? Is the stablecoin compliant in the jurisdictions your business operates in?

Stablecoin regulation helps determine whether your payment rails stay intact. Unregulated stablecoins are more likely to get delisted or frozen with little warning, leaving the business with little recourse.

Ease of access

Can your business easily buy, sell, and move this stablecoin through the exchanges, banks, and payment platforms you already use?

A stablecoin that’s hard to access or convert adds unnecessary friction, defeating the purpose of making payments quicker and more seamless.

Chain availability

Is the stablecoin natively issued across multiple blockchain networks, or is it limited to just one?

This affects who you can pay and how. A stablecoin that’s only available on a single chain limits where you can send it and can increase your transaction costs.

Distribution and ecosystem support

Which wallets, exchanges, and platforms already support it? Is it cheap and easy to move on the rails your business uses?

In payments, distribution matters as much as the mechanics. For example, PYUSD grew through its direct access to PayPal’s merchant network, while USDT dominates on the Tron blockchain because Tron offers fast, low-cost transfers. Even a stablecoin with strong fundamentals will struggle to gain real payment traction if it’s not already supported by businesses, wallets, and payment providers.

Real-world payment adoption

Is it being used for B2B settlement, payroll, and treasury operations, or primarily as a trading asset?

Widespread adoption in commercial payment is a strong signal that the stablecoin has the infrastructure, liquidity, and counterparty support needed to work reliably as a payment tool.

6 Top Stablecoins for Business Payments in 2026

Now that you know what to look for in a stablecoin, here are our top 6 top stablecoins for business payments.

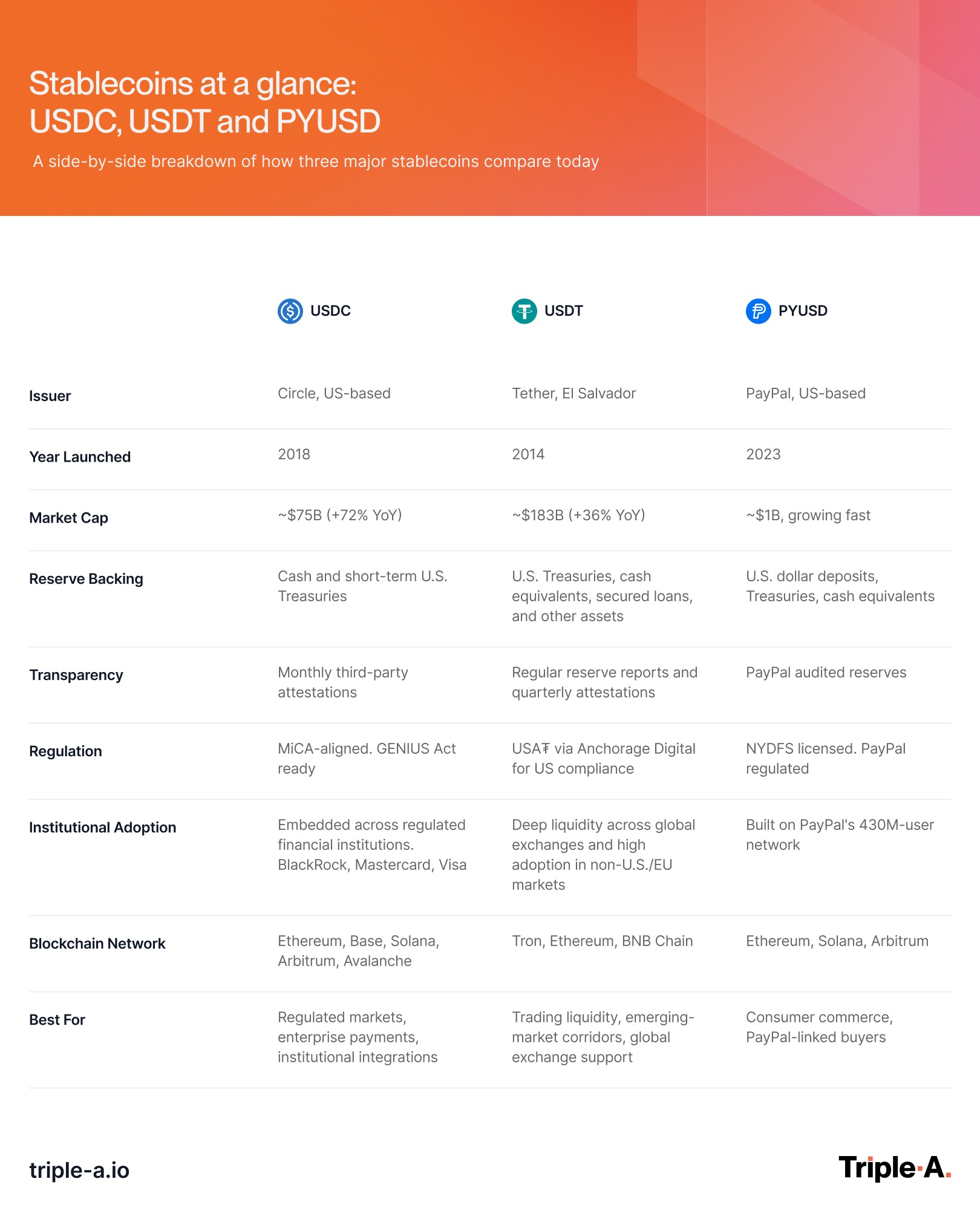

1. USDC (USD Coin)

Best for regulated markets

Issued by: Circle | Pegged to: USD | Market cap: ~$77B | Chains: 30+

USDC is the compliance-first stablecoin, which makes it our number one option for enterprise payments. Circle publishes monthly attestation reports verified by Deloitte, with reserves held in cash and short-term US Treasuries. As of 2026, USDC is registered across more than 30 chains, including Ethereum, Solana, Base, Arbitrum, and Avalanche, and holds full regulatory recognition under the EU’s MiCA framework. It’s also embedded in both Visa’s and Mastercard’s settlement rails — signalling how deeply it’s been adopted into mainstream financial infrastructure.

In the US, USDC consistently meets the reserve and licensing standards set by the GENIUS Act.

Circle’s Cross-Chain Transfer Protocol (CCTP V2) makes USDC movement between chains faster and more capital-efficient than most alternatives — a significant operational advantage for payment teams running multi-chain flows.

All this means that USDC has become the default choice for businesses operating in regulated markets, building on traditional finance rails, or requiring a clean audit trail for compliance. It’s also the stablecoin most commonly specified by regulated financial institutions, fintech platforms, and enterprise treasury systems.

It’s worth noting that while the USDC experienced a brief depeg during the Silicon Valley Bank collapse in 2023, it recovered within days and Circle has since hardened the reserve structure.

See how USDC compares to USDT in detail: USDC vs. USDT.

2. USDT (Tether)

Best for liquidity and market reach

Issued by: Tether Limited | Pegged to: USD | Market cap: ~$185B | Chains: 15+

USDT is the largest stablecoin on the market by a wide margin. It is available on more than 400 exchanges with roughly $185 billion in circulation — about 60% of the total stablecoin market.

This means that USDT has deeper liquidity and a broader market reach than any of the alternatives. For businesses that prioritize settlement speed, and need to move large volumes across emerging-market corridors, no other stablecoin matches USDT’s network depth. Many counterparties in Asia, Latin America, and emerging markets prefer to pay or settle in USDT, making it difficult to ignore if you’re building global payment operations.

When it comes to compliance and transparency, Tether publishes daily reserve reports and quarterly attestations and has expanded its disclosures in recent years. USDT’s reserve composition includes a mix of US Treasury bills, cash, and short-term securities. It remains the preferred stablecoin for high-volume cross-border payment flows, particularly in corridors where USDC has less reach.

For businesses with strict audit or compliance requirements, USDC’s monthly attestation model may be a better structural fit. However, many enterprise payment stacks hold both: USDC for regulated flows, and USDT for liquidity-sensitive corridors. In practice, many businesses use USDT where global liquidity offers advantages, but hold it briefly rather than as a long-term treasury reserve.

3. PYUSD (PayPal USD)

Best for getting started with stablecoins

Issued by: Paxos (for PayPal) | Pegged to: USD | Market cap: ~$2.85B | Chains: Ethereum, Solana, Arbitrum, Stellar

PYUSD is PayPal’s dollar stablecoin, issued by Paxos and backed 1:1 by USD deposits and US Treasuries. Paxos operates under a New York Department of Financial Services (NYDFS) trust charter. This standard requires full reserve backing, a guaranteed redemption at full face value, and monthly attestations.

The main value of PYUSD is its direct integration with PayPal’s commercial infrastructure, giving users access to a global network of hundreds of millions of merchants and consumers that processed $1.79 trillion in payment volume in 2025. Being tied to a trusted brand also makes it easier for CFOs to get buy-in from their boards or audit committees.

For e-commerce merchants, marketplace operators, or platform-based disbursements already on PayPal’s platform, PYUSD’s stablecoin layer connects directly to existing payment workflows. PYUSD is also part of Mastercard’s stablecoin settlement network, alongside USDC and RLUSD, enabling intraday, weekend, and holiday card settlement.

Outside the PayPal ecosystem, liquidity is more limited than USDC or USDT for very high-volume settlements. Within the PayPal context, however, PYUSD is a practical on-ramp to stablecoin payments for businesses starting from traditional payment infrastructure. It’s also growing fast. In one recent 30-day window, its supply increased 16.66% compared to USDT’s 1.02%.

4. USDG (Global Dollar)

Best for businesses building stablecoin payment products

Issued by: Paxos | Pegged to: USD | Market cap: ~$2.75B+ | Chains: Ethereum, Solana, Ink

USDG is designed specifically for enterprise-grade payments with a compliance-first architecture. Paxos’s Global Dollar Network operates USDG on a revenue-sharing model, allowing institutional partners that hold and distribute USDG to earn a portion of the yield generated by the reserves.

That is what sets USDG apart. It’s designed for businesses embedding stablecoin functionality into their products, not just using stablecoins for payments.

Paxos is one of the most regulated stablecoin issuers in the world. It operates under a NYDFS trust charter under the New York Department of Financial Services, is regulated by MAS in Singapore, and is aligned with MiCA requirements in the EU.

USDG has grown quickly, crossing $2.75 billion in circulating supply in early 2026. It has over 100 network partners, and has been included in Mastercard’s stablecoin settlement set. While it may not yet be an essential stablecoin for every business, it could be a strong, regulated option to add as your stablecoin strategy matures.

USDG’s exchange footprint and liquidity depth are still maturing relative to the market leaders. For high-volume settlement needs, you should verify that it has the available liquidity for the payment corridors you use.

5. RLUSD (Ripple USD)

Best for Ripple-native payment flows

Issued by: Ripple Labs | Pegged to: USD | Market cap: ~$1.7B | Chains: XRP Ledger, Ethereum

RLUSD has been built for institutional cross-border payments and enterprise settlement, not retail trading, and its adoption trajectory reflects that positioning. Unlike more general stablecoins, RLUSD is designed to integrate directly into the Ripple. RLUSD has a market capitalization of $1.7 billion and is fully regulated under a NYDFS charter. Integrations by Deutsche Bank and LMAX Group among others are helping to drive adoption on institutional payment rails, not just exchanges. Similarly, BlackRock uses RLUSD for its BUIDL tokenized fund, and Mastercard has added RLUSD to both its stablecoin settlement network and its AI-agent payment infrastructure.

RLUSD operates on both the XRP Ledger and Ethereum — the two most relevant settlement rails for enterprise flows. RLUSD is an obvious choice for businesses already using Ripple’s existing network, particularly given XRP Ledger's settlement speed. For others, however, the other options on this list may offer better advantages.

6. EURC (Euro Coin)

Best for European payment corridors

Issued by: Circle | Pegged to: EUR | Market cap: ~$450M | Chains: Ethereum, Solana, Avalanche, Base

EURC is Circle’s euro-denominated stablecoin with over 50% of the euro stablecoin market. For businesses operating in Europe, settling invoices in euros, or serving EU-based clients, EURC eliminates the FX conversion step that USD stablecoins require.

EURC is also the most regulatory-ready EUR stablecoin available: fully MiCA-compliant and attested monthly by Grant Thornton under the same rigorous standards Circle applies to USDC.

Stablecoin comparisons for retail traders often overlook EURC, but for B2B payment teams with European exposure, it deserves a place in the stack. EURC keeps payment flows denominated in euro from origin to settlement, reducing exchange friction, simplifying reconciliation, and aligning businesses across the eurozone.

Other non-USD options

EURC isn’t the only non-USD stablecoin gaining traction. Businesses that want to avoid unnecessary FX conversion are making use of more euro, real, yen, Canadian dollar and other currency-backed stablecoins.

For example, the yen-pegged JPYC crossed 350 billion yen in transaction volume within months of being launched in 2025. Brazil’s BRLA is processing roughly $400 million a month on local instant-payment rails. And Singapore’s regulatory framework already supports stablecoins pegged to a range of G10 currencies.

While the dollar still overwhelmingly dominates the market, more and more local-currency stablecoins are gaining regulatory backing — offering businesses with non-European and non-USD exposure more options to avoid unnecessary conversions.

What About USDe and DAI?

You may have also come across recommendations for USDe and DAI in your stablecoin research. However, for business payments, these belong in a different category.

USDe (Ethena) holds its dollar peg through a complex trading strategy involving derivatives, rather than being backed by cash or Treasuries. It’s grown to roughly $5.9 billion in circulating supply, making it the third-largest stablecoin by market cap. That said, it’s also been barred from the EU under MiCA, and briefly lost its peg during a market stress event in October 2025. While it’s an interesting financial product, it’s more risky for paying vendors or running payroll than a straightforward dollar-backed stablecoin.

DAI is backed by other cryptocurrencies rather than cash. Because crypto prices can swing significantly, DAI holds more collateral than it issues, to provide a buffer against fluctuations. It currently sits at roughly $4.4 billion in market cap. As a decentralized protocol with no single issuer, it also has no path to MiCA authorization in the EU. This gives it a risk profile that treasury teams may be uncomfortable with.

How to Choose the Right Stablecoins for Your Business

Most businesses end up holding two or three stablecoins rather than one. The right stablecoins depend on what your payment stack actually needs to do.

Here’s a practical framework:

Regulated markets and compliance: USDC – Monthly attestations, MiCA compliance, a clean audit trail, and broad acceptance among regulated counterparties.

Maximum liquidity and global reach: USDT – The deepest market depth and strongest adoption for high-volume cross-border flows and emerging-market corridors.

Getting started with stablecoin payments: PYUSD – Direct integration with PayPal’s existing ecosystem.

Building stablecoin payment products: USDG – A revenue-sharing model and multi-jurisdictional licensing make it a strong fit for fintechs and payment platforms.

Businesses using Ripple: RLUSD – Built specifically for Ripple’s payment network, with strong institutional integrations.

European payment corridors: EURC – MiCA-compliant for native euros settlement, eliminating unnecessary FX conversion.

In practice, many companies hold more than a single stablecoin. USDC often serves as the default for domestic and compliance-sensitive flows, while USDT provides liquidity for global settlement. You can then add PYUSD, RLUSD, EURC, or USDG to fit your specific needs and circumstances. Building your payment stack in this way gives you more resilience and flexibility than relying on a single stablecoin for all cases.

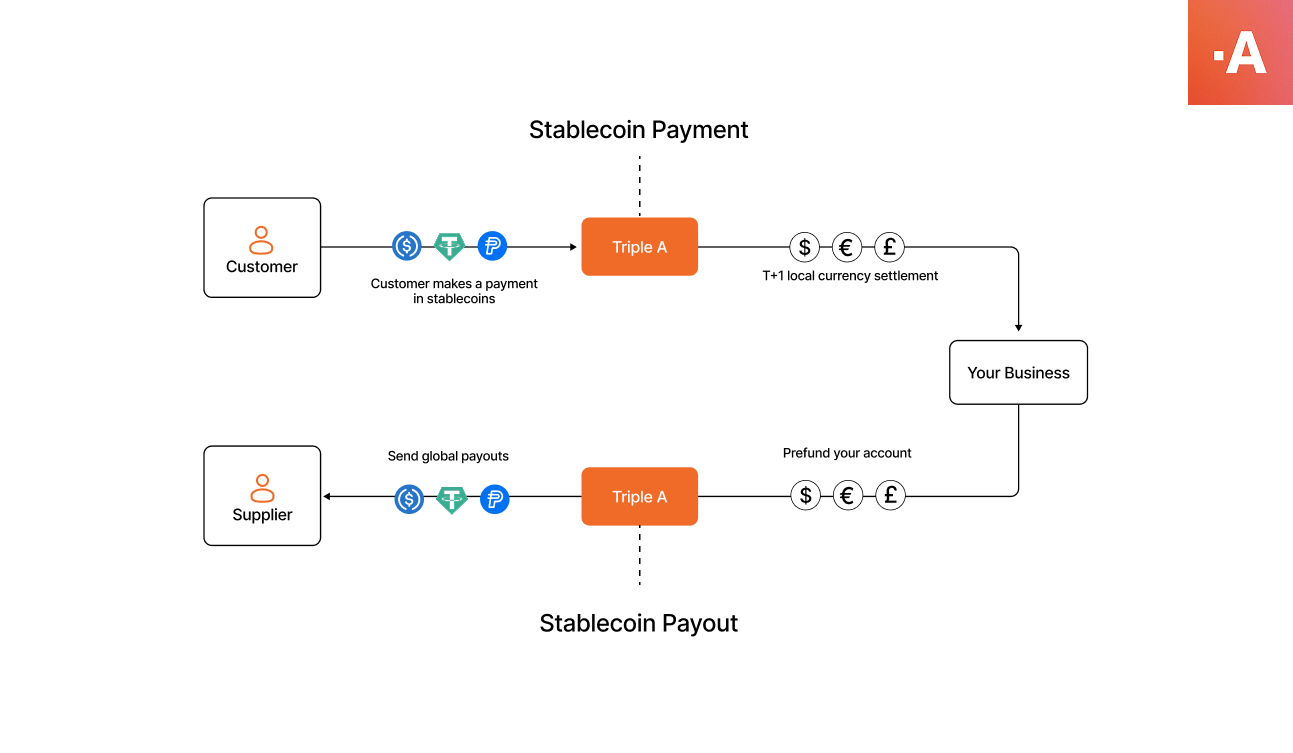

How Stablecoin Payments Work in Practice

Choosing the right stablecoin is only half the equation. The other half is who you trust to move it.

Every stablecoin on this list has its own operational rules, supported networks, and compliance requirements that can change over time. Regulations shift, exchange support changes, and what works in one country can break in another. Most businesses don’t want to track all of that themselves, and they shouldn't have to.

This is where a stablecoin payment infrastructure provider can help. Rather than managing wallets, blockchain networks, and compliance internally, you can rely on infrastructure designed to handle that operational complexity. With Triple-A, businesses receive settlements in their local currency, while the conversion, wallet management, and compliance are handled by the infrastructure. You get the speed and cost advantages of stablecoin payments without the burden of running them yourself.

The stablecoins covered in this guide are the ones most commonly used for modern business payments. The right mix for your business depends on your corridors, volume, and compliance requirements. And with the right infrastructure, you can handle your stablecoin portfolio without having to manage the complexities yourself.

Ready to add stablecoin payments to your stack? Get in touch with our team.