Stablecoin Regulations: What Every Business Needs to Know In 2026

Stablecoin Regulations: What Every Business Needs to Know In 2026

For a long time, stablecoin regulation was something businesses could monitor from a distance.

While frameworks were “proposed,” enforcement was selective at best. If you were processing payments in stablecoins, you could largely operate without worrying too much about which rules applied to you or your provider.

That era is over. In 2025, crypto exchanges faced over $1 billion in fines for money laundering and sanctions violations, with many of them tied to transaction monitoring failures and licensing lapses. Likewise, under the strict liability standard enforced by the U.S. Treasury’s Office of Foreign Assets Control (OFAC), which now explicitly extends to stablecoin payment infrastructure, businesses can be held responsible for sanctions violations even if they had no knowledge of them.

The rules governing stablecoin payments have fundamentally changed and the consequences of getting it wrong are more costly than ever. Therefore, for any business that pays or gets paid in stablecoins, it’s now crucial to ensure your payments provider is built for compliance.

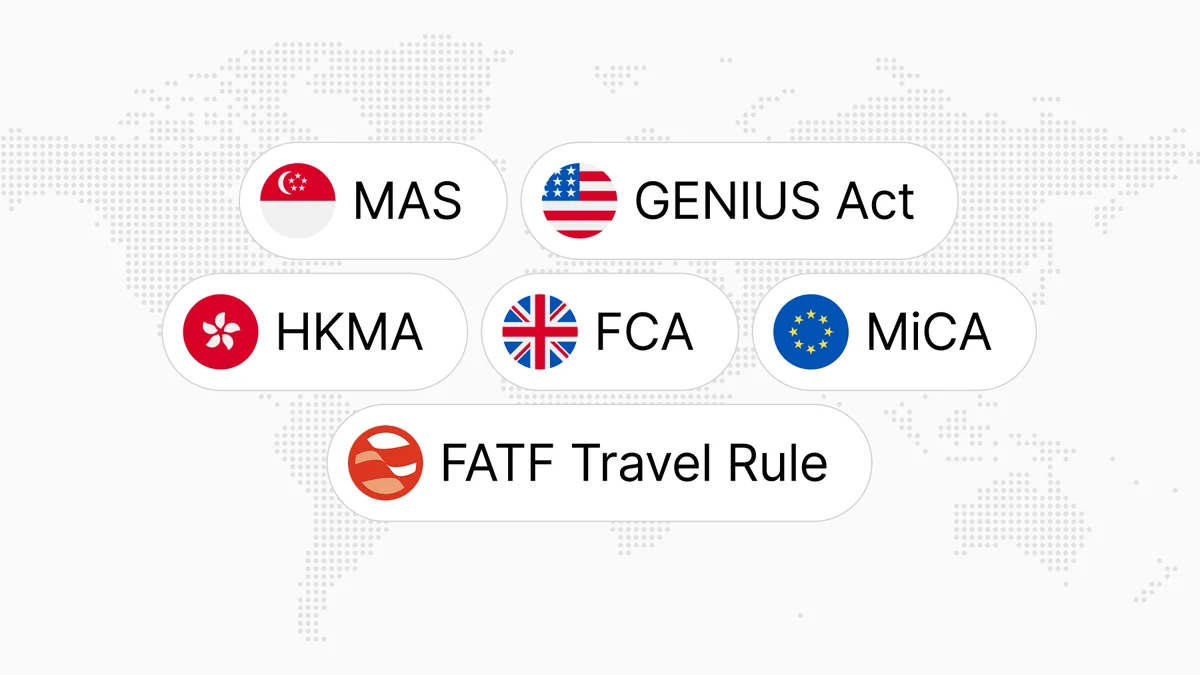

At Triple-A, we operate under licenses across the US, EU, Singapore, Canada, and South Africa. In this article, we cover what regulation means for your business, and dive into the major regulatory frameworks now in force, including the GENIUS Act, MiCA, and PS Act. We’ll discuss what these regulations require, how they’re being enforced, and what to look for in a payments partner that’s built to meet them.

Brief Overview of What’s Changed

In every major market where stablecoins move money at scale, the regulatory environment has fundamentally changed.

- In 2024, the EU’s Markets in Crypto-Assets regulation (MiCA) came into full force, requiring stablecoin issuers to hold banking-grade licenses or face delisting from European exchanges. This led to USDT, the world’s most widely used stablecoin, being removed from some platforms, such as Coinbase Europe, Kraken, and Binance’s EEA.

- In 2025, the U.S. passed the GENIUS Act, the first federal framework for payment stablecoins. The Act brought stablecoin issuers into a formal licensing regime, with requirements around 1:1 reserve backing, public disclosures, AML and sanctions compliance, holder protections, and restrictions on yield-bearing stablecoins.

- The UAE has also moved from regulatory experimentation to active supervision. The Central Bank of the UAE’s Payment Token Services Regulation is now in force, setting licensing and registration requirements for payment token services, while Dubai’s Virtual Assets Regulatory Authority (VARA) has developed a dedicated virtual asset framework, including rules for virtual asset issuance and fiat-referenced virtual assets.

- The UK is also finalising its stablecoin framework. In 2025, the FCA consulted on rules for issuing qualifying stablecoins and safeguarding cryptoassets, while the Bank of England published proposals for the regulation of sterling-denominated systemic stablecoins used in payments. Final rules are expected to shape how stablecoins can be issued, backed, safeguarded, and used in UK payment systems.

- In Singapore, the Payment Services Act has regulated payment services, including digital payment token services, since 28 January 2020. The more recent shift came in August 2023, when the Monetary Authority of Singapore (MAS) finalised a dedicated framework for single-currency stablecoins issued in Singapore, adding specific requirements around reserve backing, redemption, disclosures, and prudential standards.

- Japan also moved early. In June 2023, amendments to the Payment Services Act brought fiat-pegged, redeemable stablecoins under a dedicated “Electronic Payment Instruments” regime. Issuance is limited to regulated entities such as licensed banks, trust companies, and registered money transfer service providers, making Japan one of the clearest examples of a bank-led stablecoin framework.

What Stablecoin Regulation Means for Your Business

The current regulatory frameworks have direct operational and financial consequences for any business that touches stablecoin payments.

Here’s what’s actually at stake:

Your payment rails can break overnight

The 2024 USDT delistings were more than a simple exchange problem. Businesses that had built payment flows on non-MiCA-compliant rails woke up to broken infrastructure without any warning or grace period.

For businesses that relied on USDT rails in Europe, that meant transactions rejected at the point of payment, settlement windows missed, and customers who couldn’t complete purchases. There was also no clear timeline for resolution.

The same risk now exists in every jurisdiction with an active framework. A provider that loses its license or operates without one can take your payment operations down with it.

Your transactions determine your legal exposure

Under OFAC’s strict liability standard, your business can be held responsible for sanctions violations even if you had no knowledge of them. That means every transaction you process creates legal exposure, regardless of who facilitated it. If your payments provider routes a transaction through a sanctioned entity or jurisdiction and doesn’t catch it, you can still be held liable for that transaction.

In 2025, OKX was fined $504 million after pleading guilty to U.S. anti-money laundering violations, including operating without the required money transmission licence. The businesses using OKX for payments did not pay the fine in that case, but the lesson is clear: your payment infrastructure is part of your compliance risk. As regulation tightens, companies need to know who is processing their transactions, where those transactions flow, and whether the provider has the controls to withstand regulatory scrutiny.

The stablecoin on your balance sheet is only as good as its reserves

If your business holds stablecoins for treasury, payroll, or settlement purposes, the GENIUS Act’s reserve requirements affect you directly. A stablecoin backed exclusively by cash and short-dated Treasuries carries a fundamentally lower risk profile than one backed by a mix of secured loans and other assets.

If USDT depegged tomorrow, a business holding $500,000 in USDT for payroll or supplier payments would absorb that loss directly. The GENIUS Act’s strict reserve requirements exist precisely because that scenario has happened before and the businesses holding the stablecoin had no recourse.

The Travel Rule puts documentation obligations on you

The Travel Rule, which requires originator and beneficiary information to travel with every qualifying transfer, is now enforced across MiCA, the GENIUS Act, and MAS frameworks. In practice, this means a wire-equivalent paper trail for every qualifying transfer. If your provider can’t produce that documentation, any receiving banks and payment institutions in MiCA or GENIUS Act jurisdictions can reject the transaction outright.

Regulatory scrutiny is shifting from issuers to the businesses that use them

In the past, enforcement focused on exchanges and issuers. But now, regulators are increasingly looking at the full payment chain, which means that businesses can be exposed if they can’t demonstrate that they have vetted their provider’s compliance.

Due diligence on your payment partner is now a compliance obligation, not a best practice. The question isn’t whether your provider is compliant: it’s whether you can prove you asked.

01

Are you licensed in the jurisdictions where my business operates?

A provider registered in one country isn’t automatically compliant in others. Ask for their specific licenses and verify them.

02

How do you handle sender and recipient information on transfers?

According to FATF Travel Rule requirements, your provider has to collect and share identifying information about both the sender and the recipient for every qualifying transfer. Ask how they handle this and what happens if information is incomplete.

03

Do you screen transactions against sanctions lists in real time?

Under global compliance standards, real-time screening is mandatory and crucial.

04

How do you comply with the Travel Rule?

Ask which network they use to transmit the information and how they ensure the security and encryption of the data during transmission.

05

What happens when a transaction triggers a compliance alert?

A provider with a well-defined compliance program must have a clear process for this. Vague answers here are a red flag.

Global Stablecoin Regulations

Stablecoin regulation has moved fast. In the span of two years, the world’s major economies went from debating frameworks to enforcing them. Here’s where the key regulations stand today.

U.S. Regulations: The GENIUS Act

On July 18, 2025, President Trump signed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act into law. The new legislation passed with overwhelming bipartisan support, with a 68–30 win in the Senate and 308–122 win in the House. This established the first federal framework in the United States specifically governing stablecoins used for payments.

The Act will take effect on January 18, 2027, or 120 days after regulators finalize their implementing rules — whichever comes first.

Core Requirements for Stablecoin Issuers

- 1:1 reserve backing. This backing must be from a narrow set of permitted assets, such as cash, U.S. government securities, and equivalent instruments. Loans, crypto assets, and corporate debt are not allowed.

- Monthly public disclosures. These disclosures need to identify the assets being used to back up their reserves and be independently attested.

- AML and sanctions compliance. Stablecoin issuers are now treated as financial institutions under the Bank Secrecy Act and must meet the same compliance standards as licensed financial institutions. This includes screening against OFAC lists, which cover sanctioned countries, entities, and individuals that U.S. businesses are prohibited from transacting with.

- Holder protections. Stablecoin holders must take priority over all other creditors in the event of issuer insolvency or bankruptcy.

- Absolutely no yield. Issuers are prohibited from paying interest or returns to holders simply for holding a stablecoin. This closes the door on yield-bearing stablecoin products from licensed issuers.

- No misrepresentation. Issuers cannot use names or language that imply their stablecoin is federally insured or government-backed.

The Act also establishes three pathways for getting licensed, depending on the size and type of issuer.

- Subsidiaries of federally insured banks can apply through their primary federal regulator.

- Nonbank issuers can apply for a federal license directly through the OCC (Office of the Comptroller of the Currency).

- Smaller nonbank operators with under $10 billion in outstanding stablecoins can opt into a state regulatory regime, provided their state’s framework is certified as substantially similar to the federal one.

Any state-licensed issuer that grows beyond that threshold must transition to federal oversight.

Foreign stablecoin issuers are not locked out of the U.S. market, but they must register with the OCC and demonstrate compliance with standards comparable to U.S. requirements. This matters for businesses using non-U.S. stablecoin infrastructure: the issuer your payments run on needs to be either domestically licensed or formally registered as a foreign issuer.

The CFTC has also moved in parallel, launching an initiative to promote compliant stablecoins and tokenized collateral in derivatives markets — a signal that stablecoins are becoming integrated into mainstream financial infrastructure, not just payments.

For businesses, the practical implication is clear: any stablecoin used for commercial payments in the U.S. must now be issued by a licensed, federally supervised entity operating under strict reserve, disclosure, and AML requirements. The era of unregulated stablecoin issuers in the U.S. market is over.

EU Regulations: MiCA

While the U.S. was passing the GENIUS Act in 2025, the EU’s Markets in Crypto-Assets (MiCA) regulation had already reached full enforcement by the end of 2024.

Core Requirements for Stablecoin Issuers

- 1:1 reserve backing. Reserves must be held in high-quality liquid assets, such as cash or cash equivalents, in segregated accounts with a third-party custodian. They cannot be mixed with the issuer’s own funds.

- Regular reports on their reserves. These reports must be verified by an independent third party, giving regulators and holders full visibility into what’s backing the stablecoin.

- AML and Travel Rule compliance. The Travel Rule requires issuers and payment providers to collect and share the sender and recipient information for every qualifying transfer — the same standard applied to traditional wire transfers. This means every stablecoin transaction over the threshold must carry identifying information about the sender and the receiver that is traceable end to end.

- Holders can redeem the face value at any time. Issuers must guarantee that any holder can exchange their stablecoin for the equivalent fiat amount on demand, with no questions asked.

- Must be licensed. A company must hold either an e-money institution (EMI) license or a credit institution license to issue a stablecoin in the EU.

- Mandatory public whitepaper. Before issuing, companies must publish a document disclosing how the stablecoin works, what it is backed with, and the risks involved. Marketing materials must match the information in the whitepaper.

- Significant stablecoins face stricter rules. If a stablecoin is used widely enough to become systemically important, the European Banking Authority steps in with enhanced supervision, more frequent reporting, stress tests, and higher capital requirements.

- Personal liability for executives. If senior management is found responsible for violations, regulators can bar individuals from working in the crypto industry entirely.

Non-compliant stablecoins don’t get a grace period: they simply get delisted. The market has already learned this the hard way. USDT was progressively removed from major European exchanges, including from Kraken, Coinbase Europe, Binance’s EEA users, and more. Meanwhile, USDC, which holds full MiCA authorization through Circle’s EU entity, became the dominant compliant stablecoin by default.

If you operate in Europe or accept payments from European customers, and your payments provider isn’t MiCA-compliant, you are left exposed. However, if you have a compliant payment institution licensed in one EU member state, it can passport authorization across all 27.

Other Notable Regulations

The regulatory shift isn’t just limited to the U.S. and EU.

Singapore’s MAS framework has been the gold standard since early 2020, long before either GENIUS or MiCA existed. In fact, Triple-A was one of the first digital currency payment companies to receive an MPI license from MAS, a rigorous licensing process covering AML/CFT controls, capital adequacy, and ongoing supervisory compliance. Beyond Singapore, Japan, Canada, the UK, UAE, Hong Kong, and Australia all have active or finalizing stablecoin frameworks. Here’s where each one stands:

Key Frameworks by Jurisdiction

Please note that these frameworks cover different activities. While some apply specifically to stablecoin issuers, others govern payment services that stablecoins fall under. Dates are approximate. Verify current status with legal counsel.

How Triple-A Operationalizes Compliance

Compliance is one of Triple-A’s largest departments, second only to development and technology. That reflects a simple reality: in regulated digital currency payments, compliance is product infrastructure. It is what allows merchants to access stablecoin rails without taking on the operational, licensing, sanctions, Travel Rule, and monitoring burden themselves. As MiCA, the GENIUS Act, and other frameworks move stablecoin payments into a more heavily supervised environment, the quality of a provider’s compliance program directly affects whether payments are accepted, settled, documented, and defensible.

Built Compliant from Day One

Compliance at Triple-A has been foundational since the company’s earliest licensing work, led by Cristal He, Triple-A’s Head of Compliance, “The most fulfilling part of my role is achieving the right balance between strict compliance and business needs”. Her focus has been on building compliance in a way that supports both regulatory expectations and real-world business needs.

That approach is reflected in Triple-A’s active, multi-jurisdictional license portfolio:

- United States: Licensed/exempted as a money transmitter across 19 states, including Washington, Florida, and California, and registered as a Money Services Business with FinCEN, the U.S. Treasury’s financial crimes enforcement network.

- European Union: Licensed as a Payment Institution in France, with that authorization passported across all 30 EU/EEA member states. Also authorized under MiCA as a Crypto-Asset Service Provider, enabling regulated digital asset services across the EU.

- Singapore: Licensed by the Monetary Authority of Singapore (MAS) as a Major Payment Institution, covering merchant acquisition, digital payment tokens, and domestic and cross-border money transfers.

- Canada: Registered with Canada’s financial intelligence unit as a Foreign Money Services Business and with the Bank of Canada as a Payment Service Provider.

- South Africa: Exempted by the Financial Sector Conduct Authority (FSCA) as a Foreign Financial Services Provider.

In practice, this means that every transaction processed through Triple-A operates within a licensed and regulated environment. Triple-A’s merchants can choose to handle only local currencies and don’t have digital currencies on their books. That helps businesses get the speed and cost advantages of stablecoin rails without inheriting the regulatory burden of holding, screening, or settling digital assets themselves.

Triple-A achieves this through a licensed, regulated operating model, supported by layered AML/CFT controls across the full transaction lifecycle.

- The framework starts before a transaction is processed, covering KYC/KYB checks, document collection, identity verification, customer risk assessment, as well as name screening against sanctions lists, politically exposed persons, enforcement records, and adverse media databases.

- These checks continue after onboarding and throughout the business relationship, with ongoing screening, periodic recertification by customer risk level, and event-triggered reviews when new risk indicators appear.

- At the transaction level, Triple-A combines wallet screening, blockchain analytics, Travel Rule compliance, and real-time transaction monitoring.

- Wallets and transactions are analysed for behavioural patterns, source of funds, source of wealth, geographic exposure, sanctions exposure, and other risk signals.

- High-risk activity can be blocked in real time based on Triple-A’s internal risk scoring, while suspicious transactions are escalated to Compliance and Senior Management for review and, where required, reported to the relevant authorities.

This program is reinforced by documented policies, recordkeeping, remediation processes, employee AML/CFT training, and annual independent testing of the overall compliance framework.

This is vital as compliance in stablecoin payments cannot be reactive. It has to be embedded into every onboarding decision, payment flow, payout, and regulatory reporting obligation. Triple-A’s compliance infrastructure provides merchants with a protective layer between their businesses and the regulatory complexity of digital asset payments.

--

Stablecoin regulation is here to stay, and it is getting tighter. For businesses, this changes one thing above all else: the compliance posture of your payments provider is now a direct reflection of your own. If they’re licensed, audited, and operating under real regulatory supervision, you’re protected. If they’re not, you’re exposed.

If you’re ready to get started with compliant stablecoin payments, talk to the Triple-A team.